Blockchain Technology and Cost Transparency Revolutionizing Construction

The construction industry, a cornerstone of economic development and infrastructure, has faced persistent challenges in the realms of cost management and operational efficiency. Historically, construction projects have been mired in issues that range from budget overruns to contentious disputes regarding payment and expense allocation. In addition to these problems, stakeholders, be they project managers, investors, or regulatory bodies, have often grappled with the frustration of navigating complex and fragmented data systems that hinder timely access to reliable financial information about ongoing projects.

However, in recent years, a groundbreaking innovation has emerged on the technological horizon that holds the promise of revolutionizing the construction industry as we know it – blockchain technology. This transformative technology, which initially gained fame through its association with cryptocurrencies, is now stepping into the construction arena with the potential to bring about unprecedented levels of cost transparency, accountability, and efficiency. In the following sections, we will delve into the profound impact of blockchain technology on construction, shedding light on how it is poised to disrupt the industry's traditional norms and usher in an era of unparalleled transparency and financial efficacy.

Understanding Blockchain Technology

Blockchain technology, at its core, represents a paradigm shift in how data is recorded, and transactions are managed. It functions as a decentralized and immutable ledger, which means that it doesn't rely on a central authority or a single point of control. Instead, it operates across a network of computers (nodes) where each transaction, referred to as a block, is cryptographically linked to the previous one, forming a continuous chain. This design ensures that once information is recorded on the blockchain, it becomes nearly impossible to alter or erase, creating an exceptionally secure and transparent record of all activities within the system. While blockchain's initial prominence was largely associated with cryptocurrencies like Bitcoin, its versatility allows it to extend its transformative potential far beyond the realm of finance, finding applications in various industries, including construction.

The Current Landscape of Cost Transparency in Construction

In the construction industry, the historical lack of transparency in cost management has been a persistent challenge. Several factors contribute to this opacity:

Fragmented Data: Construction projects typically involve a multitude of stakeholders, ranging from architects and contractors to suppliers and regulatory authorities. Each of these entities often maintains its own set of records and documentation, leading to a situation where data becomes fragmented across the project lifecycle. This fragmentation makes it arduous to consolidate and verify financial information accurately.

Manual Processes: Despite technological advancements in other areas, many facets of cost management within construction still rely heavily on manual processes. These manual workflows not only introduce the potential for human errors but also impede the industry's ability to achieve real-time visibility into project finances. This lack of immediacy can hinder decision-making and contribute to cost overruns.

Limited Accountability: The complexity of construction projects, often involving numerous subcontractors and stakeholders, can make it challenging to assign clear responsibility for cost overruns or discrepancies. This lack of accountability can lead to disputes among the parties involved, further exacerbating project delays and financial uncertainties.

Blockchain: A Paradigm Shift in Cost Transparency

Here's how blockchain is poised to address the cost transparency challenges in construction:

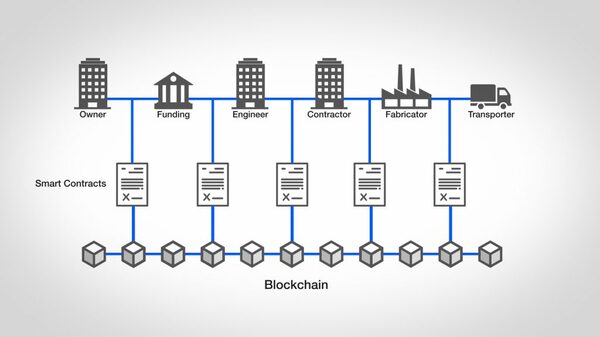

Smart Contracts Streamlining Payment Processes

One of the most transformative aspects of blockchain technology in construction is the integration of smart contracts. Smart contracts are self-executing contracts with the terms directly written into code. In construction, this means that payment schedules and conditions can be encoded into the blockchain, automating the release of funds upon meeting predefined milestones. This not only accelerates payment processes but also reduces the potential for disputes.

Immutable Records Enhancing Accountability

Every transaction recorded on the blockchain is immutable, meaning it cannot be altered or deleted. This characteristic ensures a high level of trust and accountability in financial transactions. When applied to construction, it means that once a cost or transaction is recorded, it becomes a permanent and verifiable part of the project's financial history. This reduces the likelihood of disputes and provides a clear audit trail.

Real-time Visibility into Project Finances

Blockchain provides real-time access to a comprehensive and up-to-date ledger of all financial transactions related to a construction project. This transparency allows stakeholders to monitor expenses, track payments, and assess project profitability in real-time. Such visibility empowers project managers to make informed decisions promptly, potentially preventing cost overruns and delays.

Streamlined Auditing and Compliance

Traditional auditing processes in construction can be time-consuming and resource-intensive. With blockchain, auditing becomes a more efficient and accurate process. Since all transactions are securely recorded and cannot be altered, auditors can quickly verify the accuracy and completeness of financial records. This not only saves time and resources but also enhances compliance with regulatory requirements.

Supply Chain Traceability

Blockchain also extends its benefits to the supply chain aspect of construction projects. By recording the origin, quality, and cost of materials on the blockchain, stakeholders can track the journey of materials from source to installation. This ensures the use of high-quality materials and helps prevent fraud or substitution, further contributing to cost transparency.

Case Studies: Blockchain in Construction

Several real-world examples demonstrate the benefits of blockchain technology in construction:

Proxeus and VNX Exchange Partnership

Proxeus, a Swiss blockchain start-up, partnered with VNX Exchange to tokenize a luxury apartment building in Switzerland. Through this partnership, ownership shares in the building were represented as digital tokens on a blockchain. This approach not only increased liquidity in real estate investments but also provided unparalleled transparency in property ownership and financial transactions.

IBM and Building Trust

IBM has been working on the Building Trust platform, which utilizes blockchain to increase transparency and efficiency in the construction industry. The platform offers end-to-end visibility into the construction supply chain, enabling stakeholders to track the origin and quality of materials, monitor project progress, and facilitate seamless payments.

Advantages of Incorporating Blockchain Technology in Construction

The integration of blockchain technology within the construction industry brings forth a myriad of advantages, effectively tackling the issue of cost transparency:

Minimized Disputes: The transparency and immutability inherent in blockchain substantially diminish the likelihood of disputes concerning payments, change orders, and project progression. This reduction in conflicts not only preserves valuable time but also conserves resources.

Cost-Efficiency: The automation of payment processes and streamlining of auditing procedures result in tangible cost savings for construction firms. Furthermore, the elimination of manual record-keeping significantly reduces administrative overhead.

Augmented Trust: Blockchain serves as a foundation for trust among all participants involved in a project. It achieves this by furnishing transparent and tamper-proof records encompassing all financial transactions and project-related data.

Enhanced Decision-Making: Immediate access to real-time project data empowers stakeholders to make well-informed decisions promptly. This capacity to swiftly address issues and risks helps ensure that projects remain within budgetary constraints.

Punctual Payments: Smart contracts play a pivotal role in ensuring that contractors and subcontractors receive prompt compensation when project milestones are achieved. This, in turn, bolsters cash flow and solidifies financial stability for all parties involved.

Overcoming Challenges and Adoption Hurdles

While the potential advantages of introducing blockchain into the construction sector are substantial, several challenges and considerations demand attention:

Integration Complexity: The implementation of blockchain technology entails a significant investment in technology infrastructure. Additionally, it may involve a learning curve for stakeholders who are not familiar with the technology. Addressing these integration complexities requires careful planning and effective training to ensure a seamless transition.

Data Privacy and Security: Safeguarding the security and privacy of sensitive project data within the blockchain framework is of utmost importance. Robust security measures and encryption protocols must be meticulously established and maintained to protect against data breaches and unauthorized access.

Regulatory Compliance: Adhering to industry-specific regulations and compliance standards is a non-negotiable aspect of blockchain implementation. Any blockchain solutions deployed in the construction sector must be thoughtfully designed with these considerations in mind to avoid potential legal issues and ensure full compliance.

Stakeholder Collaboration: The successful integration of blockchain in construction necessitates a high degree of collaboration and buy-in from all project stakeholders. This includes owners, contractors, subcontractors, and other relevant parties. Aligning the interests and expectations of these diverse stakeholders is critical for the technology's effective adoption and utilization within the industry.

Conclusion

Blockchain technology has the potential to revolutionize the construction industry by addressing its long-standing cost transparency challenges. Through its immutable ledger, smart contracts, and real-time updates, blockchain fosters transparency, trust, and efficiency in construction projects. The use cases and benefits of blockchain in construction are already evident, offering a glimpse into a future where disputes over payments, cost overruns, and inefficiencies are significantly reduced.

As the construction industry continues to embrace blockchain technology, it is essential for stakeholders to collaborate, invest in education and training, and overcome adoption barriers. With careful planning and implementation, blockchain can pave the way for a more transparent, cost-effective, and sustainable construction sector that benefits all parties involved.

In conclusion, blockchain technology is not just a buzzword but a genuine game-changer for the construction industry, offering a brighter future where cost transparency is no longer an issue, and projects are completed on time and within budget.

Check https://app.bidlight.com for how BidLight can help you estimate your BIM model!